If I Wanted to Buy a Home in 2026, I’d Do This

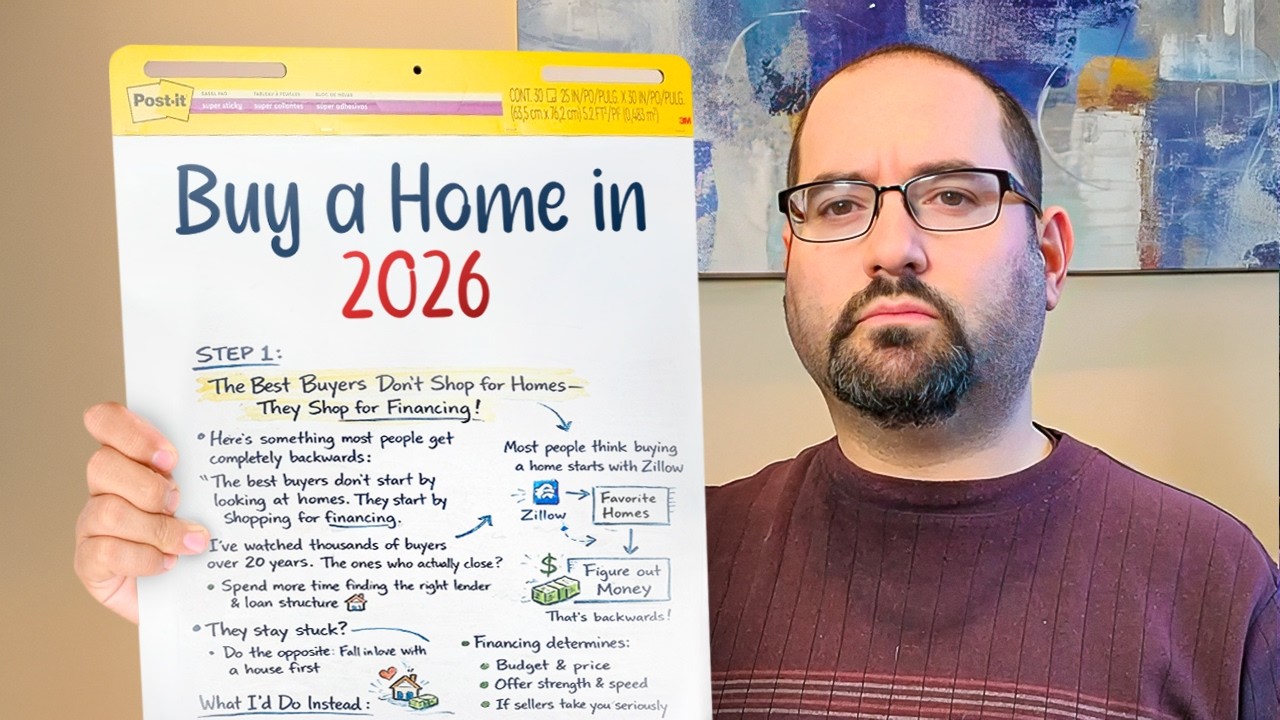

Most people start in the wrong place.

They scroll Zillow.

Fall in love with homes.

Then panic when the numbers don’t work.

I’ve seen this mistake cost people months… even years.

If I were starting from scratch today, I’d do it very differently.

Here’s what actually matters.

Mistake #1: Starting with homes instead of financing

This is where almost everyone goes wrong.

They shop for houses first.

Then try to “figure out” the money later.

That’s backwards.

Your financing determines:

What you can afford

How strong your offer is

Whether a seller takes you seriously

Without it, you’re guessing.

Get fully preapproved first.

Then shop like a buyer who can actually win.

Mistake #2: Thinking the highest offer always wins

Most buyers believe one thing.

“If I don’t offer the most, I lose.”

Not true.

Sellers don’t just want more money.

They want certainty.

A lower offer with strong financing, fast closing, and clean terms often beats a higher risky one.

If your deal feels safe…

You win.

Mistake #3: Waiting for 20% down

This one keeps people stuck for years.

They wait.

Save.

Watch prices climb faster than their savings.

Meanwhile:

Rent keeps going up

Equity stays at zero

Opportunities pass by

You can buy with 3–5% down.

The real question isn’t “Can I hit 20%?”

It’s “What’s it costing me to wait?”

Mistake #4: Trusting a weak preapproval

Not all preapprovals are equal.

Some are just:

A quick credit pull

A short phone call

Nothing verified

Sellers can spot this instantly.

A real preapproval means:

Documents submitted

Assets reviewed

Underwriting involved

When your financing is airtight…

Your offer hits differently.

Mistake #5: Building your team too late

This one kills deals quietly.

Buyers wait until they’re under contract to figure things out.

But by then, it’s too late.

Your agent, lender, and inspector are leverage.

The right team makes average offers win.

The wrong team makes strong offers fall apart.

Mistake #6: Changing finances before closing

This is where deals die.

Right before the finish line.

Buyers:

Open new credit cards

Finance furniture

Switch jobs

And everything collapses.

Until you have the keys…

You’re not done.

If you’re serious about buying, you need to see this.

I break down the exact strategy step-by-step…

Plus the mistakes that destroy deals right before closing.

Cheers,

Robert

P.S. If you want a clear plan based on your situation, this is where to start.